Conventional Refinance Loan Requirements 2021

A

conventional loan is a mortgage that meets the lending guidelines

of the Federal Home Loan Mortgage Corporation (Freddie Mac) and

the Federal National Mortgage Association (Fannie Mae).

A

conventional loan is a mortgage that meets the lending guidelines

of the Federal Home Loan Mortgage Corporation (Freddie Mac) and

the Federal National Mortgage Association (Fannie Mae).

Freddie Mac and Fannie Mae, in theory, compete with each other for

the purchase of mortgages from banks and other lenders. These two

companies are protected from default by the Federal government.

Unlike the government backed home loans, FHA, VA, and USDA mortgages

conventional loans do not require a funding fee that is paid at

settlement or financed with the loan amount. Most

loan officers encourage prospective

borrowers to refinance to a conventional mortgage because the funding

fee cost,

mortgage

insurance premium (if applicable) and other considerations.

Most loan officers encourage prospective borrowers to refinance to a conventional mortgage because the funding fee cost, mortgage insurance premium (if applicable) & other considerations. The conventional loan is used to reduce the interest rate & or term or provide cash out

Loan programs

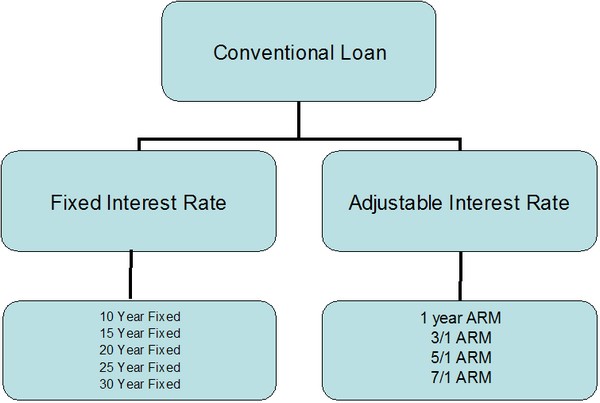

Under the umbrella of the conventional loan program are the loan "types". fixed-rate, adjustable-rate, and a combination of the fixed and adjustable-rate mortgages. Hybrid mortgages (i.e. 3/1, 5/1 & 7/1 arms) are loans that carry a fixed interest rate for a pre-determined number of years, one, three, five or seven-year terms, and then convert to an adjustable interest rate that is subject to change every 12 months. Read more about adjustable-rate mortgages

Limited cash out or cash out

There are two refinance options with the conventional mortgage,

limited refinance and cash out refinance. The limited cash out refinance

is defined as a new loan that is used to pay off an existing first

mortgage loan (including an existing home equity line of credit

in first-lien position); or for single-closing construction-to-permanent

loans to pay for construction costs to build the home, which may

include paying off an existing lot lien. Only

subordinate (2nd and 3rd) liens used to purchase the property may

be paid off and included in the limited cash out mortgage.

If there is a 2nd mortgage (i.e. home equity loan or line of credit)

and it was not used toward the purchase of the property, and the

applicant desires to payoff the second mortgage, the new loan is

classified as a "cash out" refinance. The only other option is to

obtain permission from the 2nd mortgage company to remain in 2nd

position with the new mortgage. Cash out mortgages are usually more

costly and require more equity.

Read more about limited cash-out refinance requirements.

The borrower is permitted to get cash back from a limited cash-out

refinance, but the amount borrowers receive at settlement cannot

be more than the lesser of two percent of the new refinance loan

amount or $2,000. The cash back at settlement can be built

into the new loan amount.

A cash out refinance mortgage is similar to the limited refinance

option, however, this choice permits the payoff of any unpaid principal

balance of the existing first mortgage; the payoff of any outstanding

subordinate mortgage liens of any age; taking equity out of the

subject property that may be used for any purpose.

Read more about cash out refinance mortgages.

How much can I borrow?

The following chart details the equity requirement for limited and cash out loans. For example, the limited cash out loan payoff plus closing costs (if financed) should not exceed (ideally) 95% of the appraised value. Ex. $100,000 X 95% = $95,000 (payoff + closing costs). The cash out option requires 20%% equity. That means that the loan payoff (if applicable) and closing costs should not exceed $80,000.

| Owner Occupied Residence | Number of Units | fixed-rate and adjustable-rate |

|---|---|---|

| Limited Cash-Out Refinance | 1 unit | 97% fixed-rate (conditions apply) 95% adjustable-rate |

| 2 unit | 15% (or more) - equity required for fixed-rate and adjustable-rate | |

| 3 - 4 units | 25% (or more) - equity required for fixed-rate and adjustable-rate | |

| Cash out refinance | 1 unit | 20% (or more) equity required for fixed-rate and adjustable-rate |

| Cash out refinance | 2 - 4 unit | 25% (or more) equity required for fixed-rate and adjustable-rate |

Loan term

The conventional loan terms are available for 10, 15, 20, 25, and 30-year. The FHA and VA loan programs only allows for 15 and 30-year terms. The USDA only permits a 30-year term. The interest rate is usually lower with the shorter loan term.

Second home or investment property

The conventional loan permits refinancing of second homes and investment properties (1 - 4 residential units). The FHA, VA and USDA loan programs do not permit a second home or investment property refinances.

A second home refinance is only permitted with single-family homes or approved condominiums.

| Second Home | Number of Units | fixed-rate and adjustable-rate |

|---|---|---|

| Limited Cash-Out Refinance | 1 unit | Minimum 10% equity (90% loan to value) |

| Cash out refinance | 1 unit | Minimum 25% equity (75% loan to value) |

| Investment Property | Number of Units | fixed-rate and adjustable-rate |

|---|---|---|

| Limited Cash-Out Refinance | 1 - 4 unit | Minimum 25% equity (75% loan to value) |

| Cash out refinance | 1 unit | Minimum 25% equity (75% loan to value) |

| Cash out refinance | 2 - 4 unit | Minimum 30% equity (70% loan to value) |

Here's how a conventional mortgage refinance is structured:

The loan officer starts the refinance calculation with the loan payoff and usually adds in any additional liens (i.e. lines of credit, home equity loans, etc.). The second step is to add in the closing costs, such as title insurance, settlement fees, lender's fees, etc. The lender will also add in enough property taxes for 6 to 12 months. A new homeowner's insurance policy will be required.

The lender will then divide the total refinance cost by the estimated appraised value.

For example, let's say the loan payoff is 100,000 and the closing costs and real estate taxes add up to $4,000, the total refinance cost is $104,000. And if the estimated home value is $150,000, then dividing $104,000 by $150,000, we get 69% loan to value. That's good. If the loan amount is greater than 80%, the loan would require mortgage insurance.

Monthly mortgage insurance premium

The conventional mortgage requires "mortgage

insurance" when the loan amount is greater than 80% of the appraised

value. For example, if the value of the home is $100,000 and the

loan amount is $90,000, mortgagee insurance is required. If the

loan amount is $80,000 or less, no mortgage insurance is required.

Mortgage insurance on a conventional loan should not be confused

with life insurance. The proceeds of a life insurance policy is

paid to the beneficiary on the death of the insured. Mortgage insurance

is paid to the bank or lender if there is a default on the loan.

There are several payment plans with private mortgage insurance.

The most popular payment plan is the monthly payment. The mortgage

insurance premium decreases with the equity in the home.

Conventional loans (usually) have higher loan amounts

Another advantage of the conventional mortgage is the increased

loan amounts. Each year the Federal Housing Finance Agency (FHFA)

establishes the maximum lending limit for conventional loans and

the government mortgages. For most US counties, the maximum loan

limit for conventional loans is 35% higher than the FHA mortgage.

The lending limit increases with two, three, and four-unit residential

properties. The VA single-family loan limit is the same as the conventional

loan limit for a one-unit dwelling. The VA does not have higher

lending limits for 2 - 4 unit owner occupied properties. The USDA

does not impose a lending limit, however, the USDA has other guidelines

that lower the loan amount for a refinance mortgage.

When the loan amount exceeds the lending limit of Fannie Mae and

Freddie Mac, the loan is known as a

jumbo loan. Jumbo

mortgages cannot be sold to either Fannie Mae or Freddie Mac due

to the purchase limitation. The lender holds the loan in the mortgage

portfolio or sells the loan to a lender who is willing to accept

the risk. Since there is a risk with holding on to a high-value mortgage,

the interest rate is increased.

Loans are said to "conform" when the loan amount is at or below

the Fannie Mae and Freddie Mac lending limits and meet the agency's

lending guidelines. Lenders will use term conventional conforming

loan to describe a conventional loan that meets the guidelines and

meets the lending limits set by the Federal Housing Finance Agency.

Conventional loan interest rates

You might be surprised to know that the interest rate on conventional

loans are "adjusted" based on the applicant's credit score, whether

the refinance mortgage is a limited refinance or a cash out loan.

Cash out loans cost more. Two to four-unit properties cost more,

low credit scores increase the interest rate or closing costs. Fannie

Mae calls interest rate adjustments "Loan

-Level Price Adjustments". Freddie Mac also adjusts the interest

rates based on similar factors. Fannie Mae and Freddie Mac do not

originate conventional mortgages, but purchase loans that meet their

lending guidelines. The interest rate adjustments are sent down

to the lender, who usually pass the additional cost to the borrower.

See today's interest

rates